HCA 2Q26 Pre-Announcement: Traffic Rebounds, but Mix Pressure Drives an EBITDA Guide Cut

Florida Medicaid support helped the EBITDA beat, but weaker payer and surgical mix drove the guidance cut. Our bridge implies ~$450M of pressure beyond the two disclosed assumption changes.

Bottom line. HCA’s 2Q26 preannouncement was not a broad demand miss. Same-facility admissions increased 2.5%, equivalent admissions rose 2.7%, and emergency room visits grew 3.6%, all reaccelerating from a weather- and respiratory-affected first quarter. The problem was the economics of that activity: inpatient surgeries declined 2.3%, outpatient surgeries fell 3.4%, and a rise in uninsured patients created a significant payer-mix headwind.

Preliminary revenue of $20.23 billion increased 8.7% year over year and was 3.9% above FactSet consensus. Adjusted EBITDA of $4.03 billion increased 4.6% and was 1.9% above consensus. Nevertheless, adjusted EBITDA margin declined roughly 80 basis points to 19.9%. HCA also reduced the midpoint of its 2026 adjusted EBITDA guidance by $250 million, or 1.6%, to $15.75 billion from $16.0 billion. All figures remain preliminary ahead of the July 24 earnings report.

The headline beat was not a clean measure of operating momentum

Two roughly $400 million items shaped the quarter.

First, HCA estimated that the shift from health insurance exchange (HIX) coverage to uninsured status reduced second-quarter pretax income by approximately $400 million. That amount included a $75 million increase to the company’s prior estimate of the first-quarter impact.

Second, HCA recognized approximately $400 million of incremental Medicaid supplemental payment benefit, primarily related to Florida. The benefit covered October 1, 2024, through June 30, 2026, following approval of the state’s directed payment program.

The two items were similar in size but very different in character. The Florida benefit spans multiple reporting periods and therefore includes a substantial timing or catch-up component. The exchange headwind reflects the current economics of HCA’s payer mix and is embedded in the revised full-year outlook.

To frame the sensitivity, deducting the entire $400 million incremental Medicaid benefit from preliminary adjusted EBITDA yields approximately $3.63 billion, 8.2% below the preannouncement Street estimate and 5.8% below 2Q25. We would not treat $3.63 billion as normalized because some portion of the Florida benefit may recur. The exercise nevertheless shows why the preliminary $4.03 billion should not be treated as a clean quarterly run rate.

Patient traffic recovered, but surgical activity moved in the opposite direction

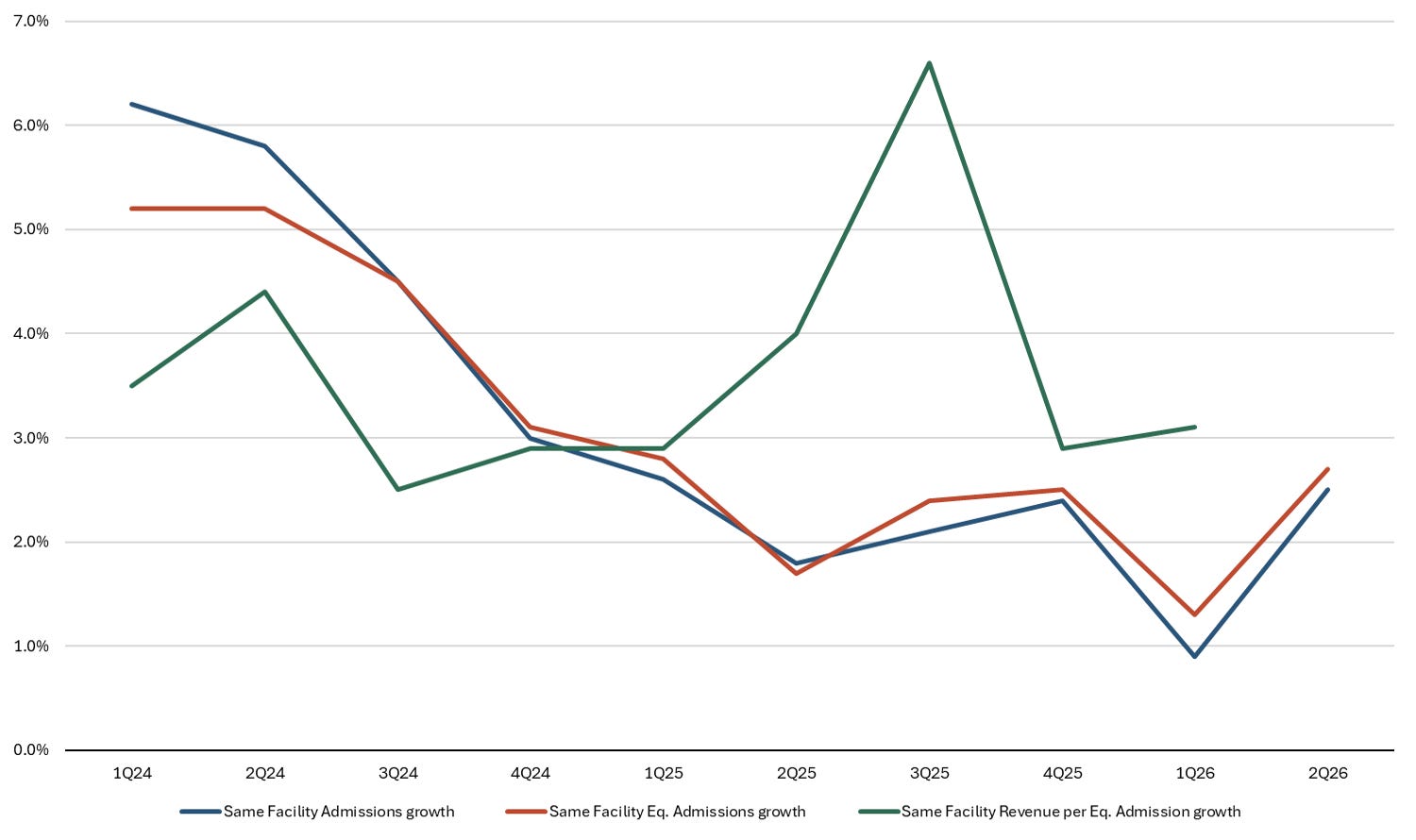

Exhibit 1. Broad patient traffic reaccelerated in 2Q26

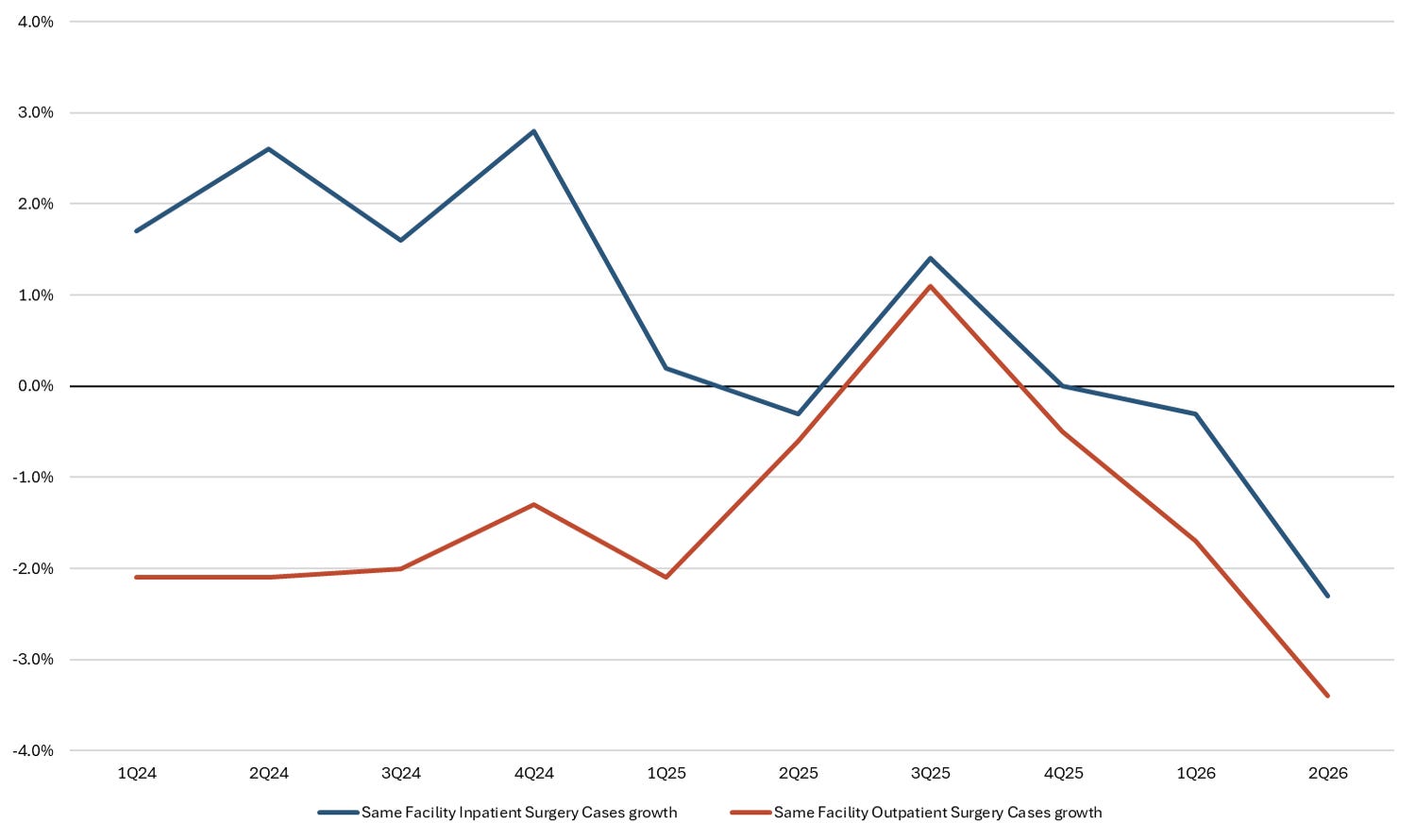

Exhibit 2. Surgical volumes weakened despite higher admissions

Exhibits 1 and 2 highlight the key distinction. Broad patient traffic improved materially from 1Q26: admissions accelerated from 0.9% to 2.5%, equivalent admissions from 1.3% to 2.7%, and ER visits from 0.3% to 3.6%. The data therefore do not point to a system-wide demand contraction.

Surgical activity tells a different story. Inpatient surgery growth deteriorated to negative 2.3% in 2Q26 from negative 0.3% in 1Q26, while outpatient surgery growth weakened to negative 3.4% from negative 1.7%. Both were the weakest readings in the ten-quarter series.

The 4.8-percentage-point gap between admissions growth and inpatient surgery growth was also the widest in the period shown. The divergence is consistent with HCA’s description of a service-mix shift: hospitals saw more patients, but fewer encounters translated into surgical cases. That effect compounds the payer issue because elective and commercially insured surgical activity generally carries more favorable economics than uninsured or lower-acuity traffic.

The guidance bridge suggests a broader reset

The midpoint of revenue guidance remains unchanged at $78.25 billion, while the adjusted EBITDA midpoint declined by $250 million. On midpoint math, that implies roughly 30 basis points of lower EBITDA margin and reinforces that the reset is about conversion and mix rather than aggregate revenue.

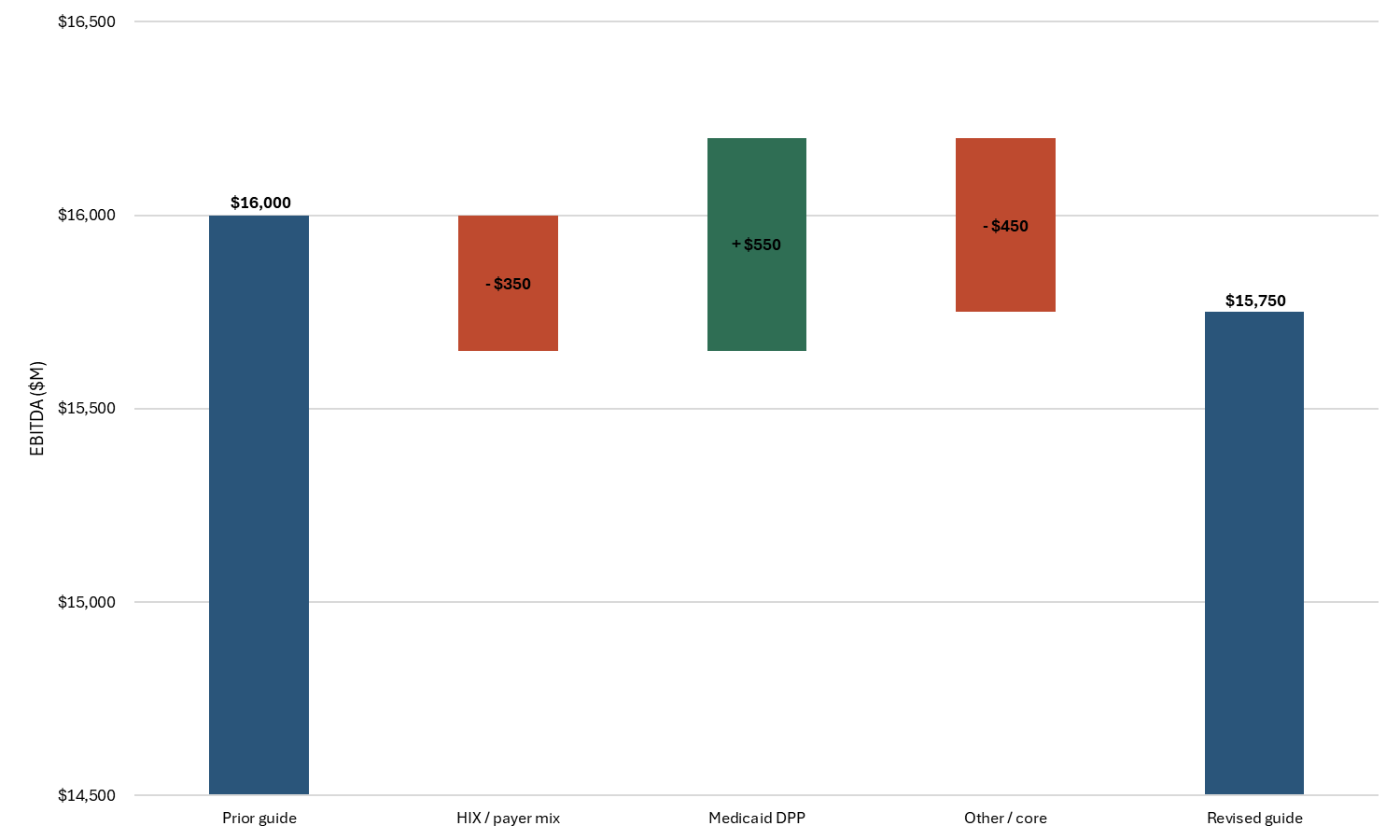

Exhibit 3. Disclosed policy changes do not explain the full EBITDA guide cut

The two disclosed assumption changes produce a net $200 million benefit, yet the adjusted EBITDA midpoint fell by $250 million. The difference is an implied $450 million residual.

This is our calculation, not a company-provided bridge, and we would not label the entire residual “core” before the earnings call. It could reflect service mix, other operating assumptions, rounding, and any unquantified change in the expected contribution from HCA’s resiliency initiatives. Still, it is the most important unanswered question in the update, particularly because HCA also cited improved expense trends.

Using the revised midpoint, HCA’s preliminary first-half results imply approximately $7.92 billion of adjusted EBITDA in 2H26, roughly 0.8% below the $7.98 billion generated in 2H25. Put differently, the midpoint no longer assumes year-over-year adjusted EBITDA growth in the second half.

The stock is discounting more than a $250 million guide cut

HCA fell 6.9% on July 14, recovered 4.2% and 1.8% over the next two sessions, and then declined 3.7% on July 17. The shares ended the four-session period down approximately 5.0% from the July 13 close, despite the intervening recovery.

At $371.18, HCA is down 20.5% year to date, 14.2% since the April 24 first-quarter report, and 31.9% from its March 9 closing high of $545.13. The latest Street snapshot shows FY26 adjusted EBITDA of approximately $15.86 billion and FY27 adjusted EBITDA of $16.54 billion. Estimates have therefore moved far less than the share price.

That disconnect suggests the market is applying a larger discount for earnings quality and visibility, rather than simply processing the mechanical $250 million guidance reduction. Investors appear less willing to capitalize Medicaid payment timing and are demanding more evidence that the deterioration in uninsured and surgical mix is stabilizing.

What matters on the July 24 earnings call

The call needs to clarify five issues:

How much of the $400 million Florida benefit was retroactive, and what portion is representative of the ongoing run rate?

What was the 2Q26 HIX headwind excluding the $75 million first-quarter true-up, and is that run rate stabilizing?

Was the surgical weakness concentrated by payer, service line, geography, or facility type?

What accounts for the approximately $450 million residual in our midpoint guidance bridge?

Does management remain confident in the previously discussed $400 million resiliency contribution?

Our preliminary conclusion is that broad hospital demand remains intact, but HCA’s earnings quality and visibility have deteriorated. The July 24 call can narrow that uncertainty, but the post-announcement price action indicates that investors are not yet willing to treat the headline 2Q26 adjusted EBITDA result as durable.