UNH 2Q26 Preview: The First Real Test of the Rebuild

Q1 was encouraging; 2Q will test whether favorable claims development, reserve conservatism and repricing are sufficient to support the 2026 recovery.

Why This Quarter Matters

UnitedHealth Group is the largest and broadest company in healthcare services. With $447.6 billion of 2025 revenue, it spans health benefits, Medicare Advantage, Medicaid, pharmacy services, care delivery, health payments and healthcare technology. That breadth makes UNH relevant to nearly every major sector debate, but the immediate investment question is narrower: has the company reset medical costs, pricing and reserves onto an earnings base investors can again underwrite?

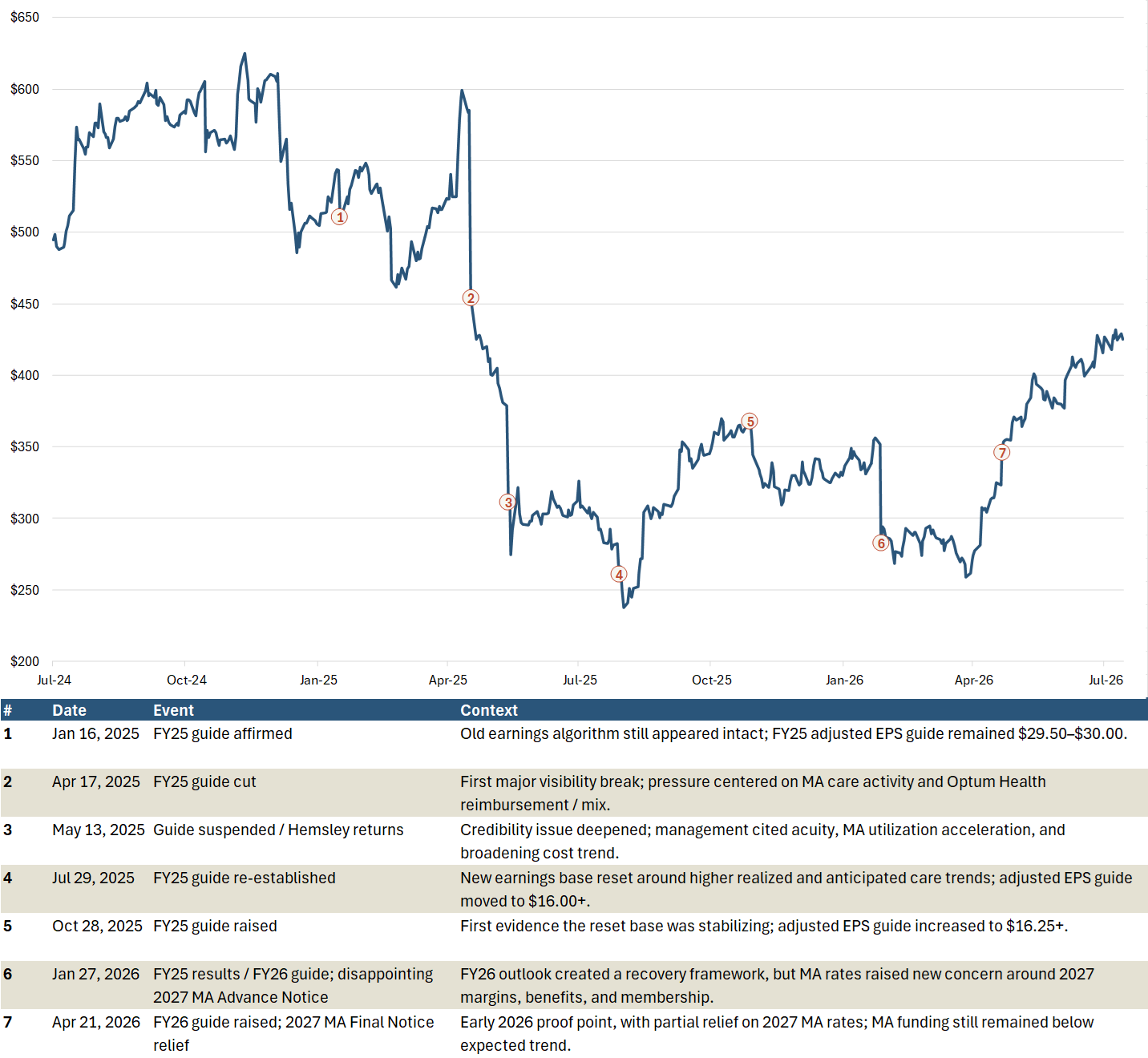

Confidence broke quickly in 2025. UNH affirmed adjusted EPS guidance of $29.50-$30.00 in January, cut the outlook in April and suspended it in May as Medicare Advantage utilization, new-member acuity and broader cost pressure exceeded expectations. By July, guidance had been re-established at only $16.00+, alongside an 89.4% MCR and unfavorable reserve development. The damage was not limited to the earnings reduction; it challenged a long-standing perception that UNH had superior forward visibility and unusually reliable guidance.

Managed-care accounting amplified the reset. Premiums and benefits are established largely in advance, while the related medical costs develop over subsequent months as claims are submitted and processed. Q1 is therefore especially estimate-dependent. When utilization and claims patterns are stable, this lag is manageable; when trend changes, a relatively small forecasting error can have a disproportionate impact on a low-margin insurer. The same annual repricing cycle can also support a rapid recovery if management correctly identifies the new cost base, although Medicaid rate adjustments typically lag.

Q1 2026 was encouraging but not conclusive. Adjusted EPS reached $7.23, the MCR improved to 83.9% and full-year guidance was raised, but the result benefited from favorable reserve development while underlying utilization remained elevated. By the second-quarter report, most Q1 claims will be substantially more developed and management will have an initial read on Q2 utilization. The print is therefore the first meaningful test of whether Q1 completed cleanly, reserves remain prudent and 2026 repricing is translating into durable margin recovery.

Exhibit 1 places that test in context, tracing the break in the prior earnings framework and the early stages of the 2026 recovery.

Exhibit 1. UNH Share Price: From the 2025 Reset to the 2Q26 Test

2Q26 Setup: Validation, Not Yet an Inflection

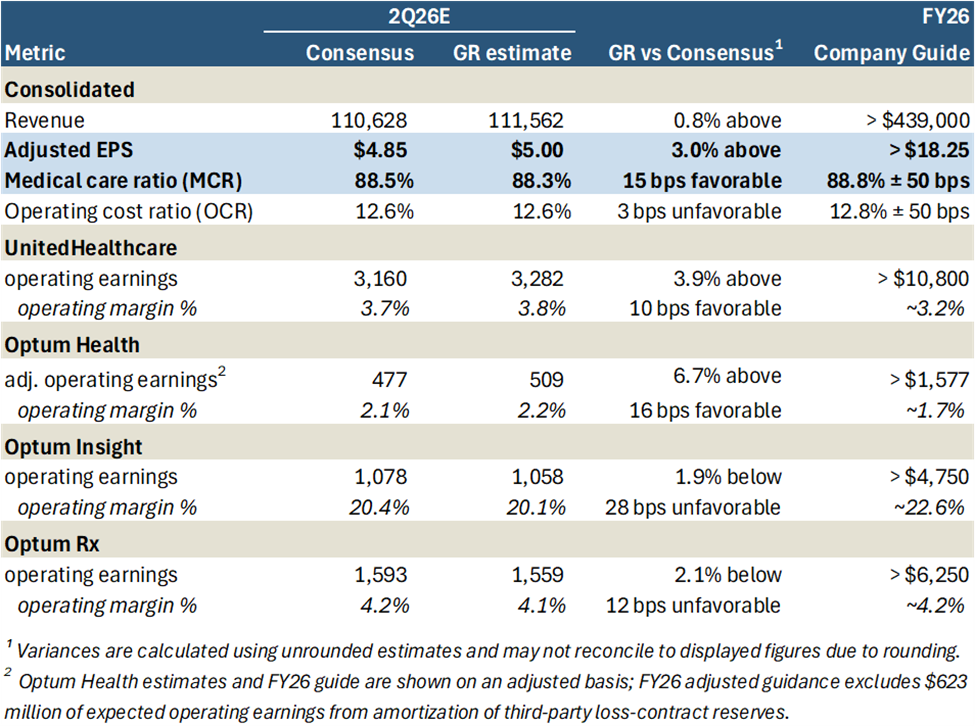

I expect 2Q26 to validate the Q1 setup rather than mark a new inflection. My estimate is $5.00 of adjusted EPS, 3% above Bloomberg consensus, on revenue of $111.6 billion. The upside is primarily MCR-driven, with UHC and Optum Health above consensus partly offset by modestly lower Optum Insight and Optum Rx estimates.

Exhibit 2. UNH 2Q26 Earnings Setup

My 88.3% MCR estimate is 15 basis points favorable to consensus and assumes modest favorable prior-period development as Q1 claims complete. It does not assume a material reduction in current medical cost trend. The expected read-through is that Q1 reserves were established prudently and that elevated utilization remains within the assumptions embedded in 2026 pricing.

At the segment level, I estimate $3.28 billion of UHC operating earnings at a 3.8% margin and $509 million of adjusted Optum Health operating earnings. My Insight and Rx estimates are slightly below consensus, reflecting their heavier second-half earnings cadence and continued investment and implementation costs.

At $5.00, first-half adjusted EPS would total $12.23, or 67% of the current $18.25 guidance floor - consistent with management’s expectation that roughly two-thirds of annual earnings will be generated in the first half. The setup is fundamentally constructive, but the stock has rerated materially since Q1. A clean validation print may support the recovery thesis without producing another outsized positive reaction; the hurdle for incremental upside is now better current-period trend, preserved reserve conservatism or a more substantive guidance raise.

Claims Completion and Reserve Quality: The Core 2Q Test

The reported MCR will matter less than the evidence beneath it: how Q1 claims completed, whether any favorability reflects reserve development or current-period trend, and what reserve position UNH carries into the second half.

Medical costs payable includes claims incurred but not yet received or processed. For recent service periods, UNH estimates the ultimate obligation using trend assumptions and completion factors - the percentage of claims expected to be visible at a given point. The company notes that billing lags can extend to 90 days and that approximately 90% of claims are known and settled within that period. A March 31 balance therefore still includes substantial estimation around February and March care activity; April and May provide a much more complete view.

That lag is benign when utilization, unit costs and submission patterns are stable, but it can create substantial earnings volatility when those relationships change. UNH’s 2025 experience is the relevant precedent: higher MA activity became visible late in Q1, then broadened as claims developed. By 2Q25, the company reported an 89.4% MCR and $70 million of unfavorable reserve development, nearly all tied to 2025 service dates.

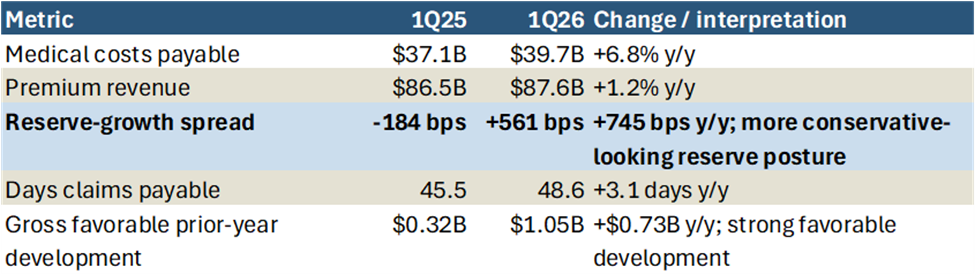

The reserve position entering 2Q26 looks materially more conservative than a year ago.

Exhibit 3. UNH Enters 2Q26 With a More Conservative-Looking Reserve Position

Panel A. Medical Costs Payable Growth Outpaced Premium Growth by 561 bps in 1Q26

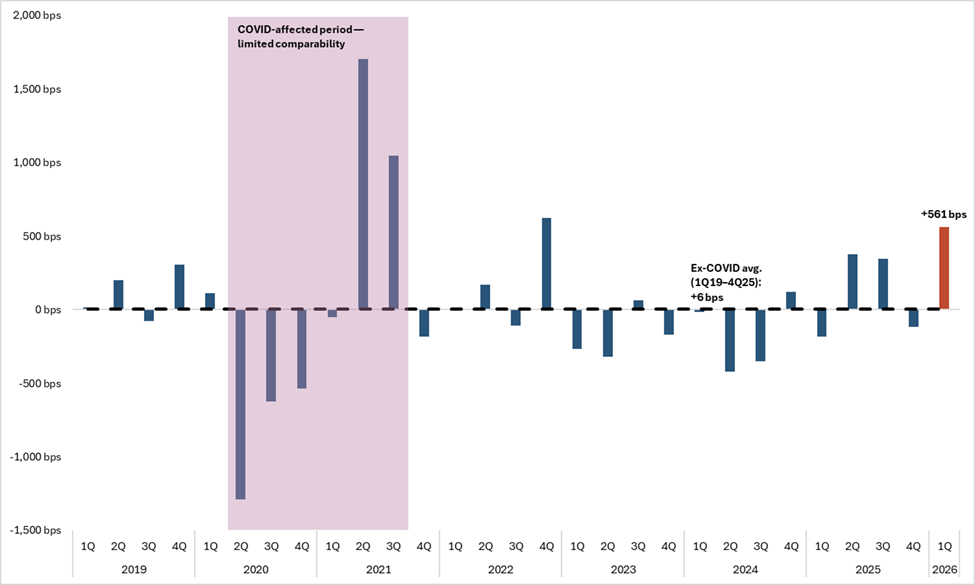

Panel B. Selected Reserve Indicators Entering 2Q26

UNH ended Q1 with $39.7 billion of medical costs payable, up 6.8% year over year, versus premium growth of only 1.2%. The resulting +561-basis-point reserve-growth spread compares with an ex-COVID historical average of +6 basis points; it is the strongest Q1 reading in my series back to 1Q19 and the second-highest non-COVID quarterly observation. DCP rose 3.1 days year over year to 48.6, while the roll-forward showed $1.05 billion of gross favorable prior-year development versus $320 million in 1Q25. Management characterized the net enterprise benefit as slightly above $500 million and said it had re-established a similarly prudent reserve position at March 31.

These metrics are supportive, not dispositive. Faster reserve growth may reflect added conservatism, but it can also reflect a larger underlying claims liability; DCP is also affected by mix, payment timing and Part D mechanics. The 2Q report therefore needs to establish three points: Q1 claims complete without adverse current-year development; current utilization remains within pricing assumptions; and the June reserve position stays prudent after any favorable development is recognized.

My 88.3% MCR estimate assumes modest favorable development and no material improvement in underlying trend. The highest-quality outcome is not simply a lower MCR, but a return to the operating pattern that historically supported UNH’s earnings consistency: cautious initial estimates, favorable claims development and sufficient reserve cushion for the seasonally more difficult second half.

UHC: Testing the Pricing Reset

UnitedHealthcare (UHC) is the clearest path to 2026 earnings recovery. At the July 2025 reset, management estimated medical costs were $6.5 billion above the original plan - $3.6 billion in Medicare, $2.3 billion across commercial and exchange products and the balance in Medicaid. The 2026 response is straightforward: price and design products around the higher cost base, accept membership contraction where returns are inadequate and restore margins before pursuing growth.

The recovery does not require medical trend to normalize; it requires pricing to remain ahead of an elevated trend environment. In MA, UNH entered 2025 with pricing based on just over 5% trend, versus an eventual 7.5% outcome. The 2026 bids assume trend approaching 10%. That is not a simple 250-basis-point cushion: roughly two-thirds of the increase reflects known provider-rate and fee-schedule changes, while the remainder accommodates less predictable risks. Residual utilization is assumed to remain high but stable.

The early evidence is favorable. Management described Q1 MA trend in the 7%-8% range against the approximately 10% pricing assumption, with modest favorability across government programs continuing through April. UHC’s Q1 operating margin increased 40 basis points year over year to 6.6%, despite MA and commercial risk membership contraction. My 2Q estimate of $3.28 billion of operating earnings and a 3.8% margin assumes that pricing alignment continues without a further trend inflection.

For Medicare, a clean quarter should preserve the expected roughly 50-basis-point margin recovery while MA membership contraction remains near 1.3 million lives. The volume loss largely reflects deliberate plan exits, benefit changes and a shift away from less manageable products. The appropriate trade-off is lower membership with adequate pricing rather than another year of volume retention at subeconomic margins. The warning sign would be attrition moving materially beyond plan without the expected margin benefit.

Commercial follows the same framework. Group trend remains near 11%, and the risk book has been repriced accordingly. At March 31, commercial risk membership was down 685,000 year over year while fee-based membership increased 750,000, reflecting both pricing discipline and migration toward self-funded products. More than 500,000 of the risk decline relates to the exchange business, which is small in the context of UNH earnings. The more important test is whether group renewals continue to close the margin gap without materially worse retention.

Medicaid remains the exception. State rate updates lag acuity and trend, limiting UHC’s ability to reprice on its own timetable. Management entered 2026 assuming 6%-7% aggregate rate increases but still expects rates to remain below trend, leaving the business in a loss position this year. April 1 and July 1 rate actions will be important, but Medicaid is unlikely to contribute meaningful upside.

The current evidence supports pricing ahead of trend in Medicare and commercial, but not Medicaid. Q2 needs to confirm that elevated utilization remains within the new assumptions, margin recovery is arriving alongside the planned membership contraction and the pricing cushion has not begun to erode.

Optum: Segment Cadence Matters

Optum is unlikely to determine whether the consolidated print is fundamentally clean; medical costs and reserves remain the primary drivers. It can, however, materially affect earnings quality. Optum Health, Insight and Rx have different seasonal profiles, so sequential growth is a poor common benchmark.

Optum Health reported $1.31 billion of adjusted operating earnings at a 5.4% margin in Q1 - more than 80% of the initial full-year adjusted floor of $1.58 billion. That is not a sustainable quarterly run rate. Following the transfer of Optum Financial to Insight, Optum Health more closely resembles a risk-bearing care-delivery business and is heavily first-half weighted. My $509 million estimate at a 2.2% margin therefore assumes a deliberate sequential decline, not renewed deterioration.

The quarter should be assessed on a clean adjusted basis. Reported 2026 guidance includes $623 million of earnings from amortizing the loss-contract reserve established in 4Q25, while adjusted guidance excludes that benefit. The accounting amortization does not represent current-year operating improvement. The key tests are no further contract or portfolio charges, no increase in the reserve and continued progress toward repricing or exiting the affected third-party contracts for 2027.

Insight and Rx are more back-half weighted, with management expecting each to generate approximately 60% of annual earnings in 2H26. At Insight, older products are being decommissioned while AI-enabled offerings are developed and commercialized. My $1.06 billion earnings estimate at a 20.1% margin is modestly below consensus; a small shortfall would be acceptable if the back-half cadence and new-product sales remain intact.

Optum Rx is absorbing implementation costs for nearly 800 new clients while UHC membership contraction reduces internal volume. My $1.56 billion estimate at a 4.1% margin is also modestly below consensus and the approximately 4.2% full-year target. The relevant read-through is whether onboarding remains on schedule and external wins, productivity and second-half volume can offset the internal membership headwind.

A clean Optum quarter may therefore appear mixed on a sequential basis: a sharp step-down at Health and only partial progress at Insight and Rx. The appropriate test is cadence. Health must deliver a clean step-down without another reset; Insight and Rx must preserve a credible second-half ramp.

Guidance and Capital Deployment

The headline question is whether UNH raises the adjusted EPS floor above $18.25. At my $5.00 2Q estimate, first-half EPS would reach $12.23, or 67% of the current floor, broadly consistent with management’s expectation that slightly under two-thirds of annual earnings will be generated in 1H26. That supports a higher floor if the operating assumptions remain intact.

The source matters more than the size. A raise supported by stable current-period trend, UHC margin recovery and clean Optum execution would de-risk the earnings base. The same increase driven mainly by reserve development, taxes or share-count accretion would be less informative. A modest raise - or even a maintained floor - could still be high quality if management preserves reserve cushion and reinvests some upside.

Capital deployment is a secondary confidence signal. Initial guidance contemplated more than $18 billion of operating cash flow, approximately $2.5 billion of repurchases and a return toward 40% debt-to-capital. Q1 delivered $8.9 billion of operating cash flow, reduced leverage to 42.9% and accelerated at least $2 billion of buybacks into the first half. Because that amount was pulled forward rather than added to the annual plan, completion is expected. The incremental signal is whether UNH raises the full-year repurchase outlook while continuing to delever.

The strongest update would show that both a higher EPS floor and additional capital return are funded by a stronger operating and cash-flow base.

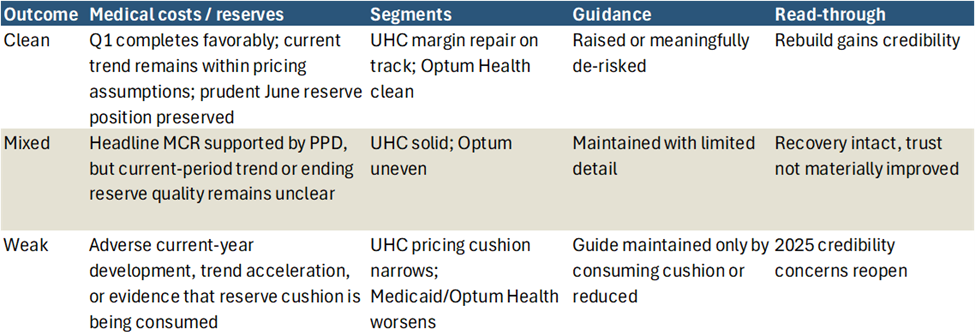

2Q Outcome Framework

Headline EPS alone will not determine the quality of the print. The key variables are Q1 claims completion, current medical cost trend, the June reserve position and the credibility of the second-half segment and guidance cadence.

Exhibit 4. UNH 2Q26 Outcome Framework

My modeled outcome is a clean print: Q1 claims complete favorably, producing an MCR approximately 15 basis points better than consensus; underlying utilization remains elevated but within 2026 pricing; UHC margin recovery stays on track; Optum Health is clean despite the expected sequential decline; and guidance is raised or meaningfully de-risked. Favorable prior-period development is part of the positive read-through, provided UNH also preserves a prudent June reserve position.

A mixed print would deliver an acceptable headline MCR but leave current-period trend, ending reserve quality or the second-half Optum cadence less clear. The recovery would remain intact, but the quarter would do little to advance the trust rebuild.

A weak print would show adverse current-year development, renewed utilization acceleration or a narrowing UHC pricing cushion. Any need to defend guidance through reserve releases or unrelated offsets would reopen the 2025 credibility concerns.

A clean print is my fundamental base case. It is not necessarily a call for an outsized positive share-price reaction: after the rerating since Q1, validation is increasingly reflected in the stock and the hurdle for incremental upside is materially higher.

Conclusion: The First Real Test

Q1 established that the recovery could be real; Q2 must show that it is durable. My base case is a clean print: favorable Q1 claims completion, elevated but controlled current trend, continued UHC margin repair, Optum performance consistent with the planned cadence and a higher or meaningfully de-risked full-year outlook.

The standard is higher than a consensus beat. Reserve development is valuable only if underlying trend and the June reserve position remain sound, while a guidance raise matters most when supported by operating performance rather than taxes, reserve releases or buybacks. Given the stock’s rerating, a clean result may validate the recovery without driving another outsized reaction, but it would materially strengthen the 2026 earnings base ahead of a fuller company view after the quarter.